The Data Architecture of Business Plans

Posts on this topic can be found in

Archive for September, 2013:

https://birkdalecomputing.com/2013/09/28/the-data-architecture-of-business-plans-part-1-an-overview/

Archive for November, 2013:

————————————————————————————–

In this article about the data architecture of business plans we will look at a standard meta-model for modeling business motivation. From an enterprise architecture prospective a business plan is the type of artifact produced at the intersection of the Business Model perspective (row two) and the Motivation aspect (column six) of the Zachman Framework, one of the most widely recognized and referenced frameworks for enterprise architecture [i]. Since models of business motivation are of most importance to business owners, this perspective is also referred to as the Business Owner perspective and the corresponding standard meta-model as the Business Motivation Model[ii].

We will explore how the standard meta-model can be extended to support the data architecture of key performance indicators (KPIs) which are popular assessors of the measurements of business performance. These measurements are often assessed in reference to the goals and objectives of the enterprise. KPIs are widely used tools in enterprise performance management (EPM) scorecards, which are in turn ubiquitous components of all three types of performance dashboards: Strategic, Tactical and Operational[iii].

The Motivation aspect addresses the question of why certain courses of action are chosen or should be chosen, why certain types of persons and organizations are important, why certain products should be more heavily invested in and why lcorrective actions need to be taken for others, why certain events are important, and why some locations are preferred over others. We will take a look at the structure of the data that describe the Motivation aspect of the enterprise from the perspective of the Business Owner. The data we will model in this article describe the entities and relationships of the data content that describes the “real world” motivations of an enterprise and thus we refer to it as metadata and the models used to understand it as meta-models.

From a Six Basic Interrogatives or 6BI[iv] point of view, when we are creating or vetting the design of a software application intended to support decision making, we seek answers to questions that will tell us “why” our client makes or should make certain business decisions and not others and “why” it is worth making the investment necessary to build (or buy) the solution we are proposing and not take another course of action. These “why” questions are just as important to ask as questions such as “what” information do we need to make the application a reality; “who” will use the application, and “how” do we measure our success.

Business Motivation Modeling

There are three business architecture models that address the Motivation aspect of the Business Owner’s perspective of an enterprise. These models are high level views that do not depend on any particular technology. In developing an enterprise performance management solution we will usually begin with one or more of the following business motivation models:

- Business Goals Hierarchy (BGH)

- Business Opportunities Hierarchy (BOH)

- Business Problems Hierarchy (BPH)

These are business architecture models designed to show details of the business vision and strategy of an enterprise. In practice the level-of-detail will vary with the scope of the engagement. If we are engaged at the top executive level then the scope is enterprise-wide. If we are engaged at the departmental or business unit level of an organization then the level-of-detail will need to be aligned with the scope of the sponsoring department or business unit in order to deliver value to the client. The scope of the goals, opportunities or problems determines the scope of the strategy. There are no well defined, hard and fast criteria for differentiating one level-of-detail from another. The levels are there as guidance to help us think more architecturally about the aspects of the business of an enterprise.

Each model depicts, in a hierarchical fashion, a different type of motivator. Each of the business motivation models is composed of a hierarchical set of “is a kind of” relationships. One approach is to start at the top with what is sometimes referred to as the apex motivator of the organization. For example, what is the organization’s single most important goal. This is most often a financial goal, but with the emerging interest in sustainability and the “triple bottom-line” may now incorporate environmental and social objectives as well.

In each model, the types of motivators depicted become more specific, finer grained, and less abstract as one progresses down the hierarchy, until reaching the “leaf node” of each branch. Another approach is to start as close to the leaf level as possible and to progress up, across and down the hierarchy all at more or less the same time. Many business analysts advocate, for reasons we need not discuss here, that this is the only practical way to actually make progress in a constrained time frame. In either case a hierarchy of motivators is created.

The apex business goal is the highest level, most abstract and most all-encompassing of all the business goals in the subject area of the BGH (Business Goals Hierarchy). The apex business opportunity is the highest level business opportunity in the BOH (Business Opportunities Hierarchy) and similarly with the Business Problems Hierarchy (BPH).

Though the three models, BGH, BOH and BPH, have virtually identical structures, goals tend to be more strategic in nature, while opportunities and problems, which are more immediate in nature, tend to be more tactical or operational. In this article we will use the Business Goals Hierarchy to illustrate the concepts behind the data architecture of business plans.

Core Business Plan Elements

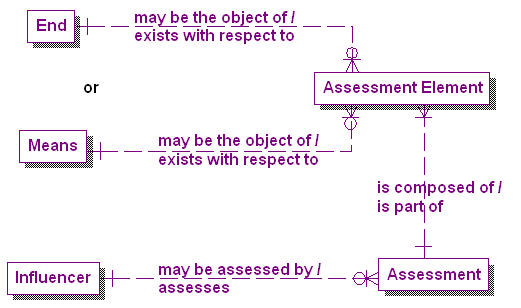

Figure 1 presents the core elements of the meta-model for business plans. Business motivation is fundamentally about four things: Ends, Means, Influencers, and Assessments. Anecdotally, Ends are where we want to get, Means are how we get there, Influencers are people, processes and technology that can influence getting there, and Assessments are how we measure if we got there.

Figure 1. Core elements of the Business Plans meta-model.

Correspondingly, in our meta-model, an End is something that an enterprise sets out to accomplish. A Means is any capability that can be called on, activated, or enforced by the enterprise to achieve an End [v]. An Influencer is anything that can produce an effect on the enterprise without apparent exertion of tangible force or direct exercise of command[vi]. The effect of Influencers on Means and Ends is determined by one or more Assessments. An Assessment is a judgment about the implications of the Influencer either with respect to one or more Means or with respect to one or more Ends. Since an Assessment can have multiple implications, each Assessment must be composed of one or more Assessment Elements. Each of these Assessment Elements then must exist with respect to either one Means or one End [vii].

In other words, the metadata describing the data architecture of business plans also describes a re-useable template for building data models to analyze, compare and improve those plans. Architecturally business plans must include data elements that represent the answers to the basic interrogatives that the plans are created to address. These basic interrogatives will include: “What is the objective that is intended to be accomplished?” – the End; “How does the process work that will get the end accomplished?” – the Means; “Who are the people and organizations that influence the process?” and “What are the technologies and other processes that will get it accomplished?” – the Influencers; and, “When was or will it be accomplished, and “How closely to expectations did it turn out to be?” – the Assessments. These are the meta-dimensions[viii] of the problem space.

Data elements that support the “When” interrogative, though not explicit in Figure 1, are very important as well, because we can accomplish our Ends through our planned Means, taking advantage of the appropriate Influencers and still fail our Assessment because the goals were not accomplished on a timely basis.

Ends

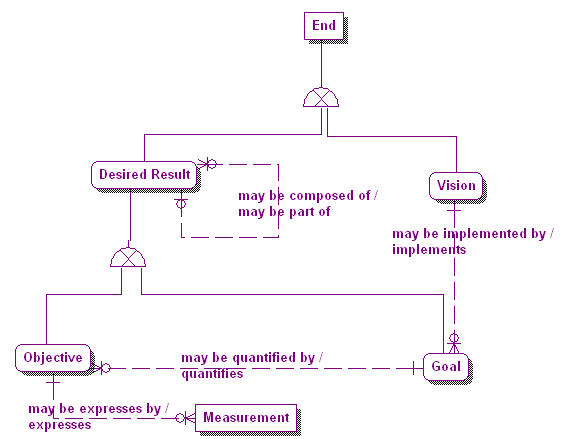

Figure 2 expands the business plans meta-model into two types of End: the Vision, which is the primary End that the enterprise sets out to accomplish, and the Desired Result, which is a state or target the enterprise intends to maintain[ix].

There are two types of Desired Result: Goals and Objectives. A Goal is a Desired Result that is a specific statement about a state or condition of the enterprise to be brought about or sustained through appropriate Means[x]. A Goal is an implementer of a Vision. That is, where a Vision describes a future state of the enterprise in general, Goals define the steps to be taken to accomplish that Vision. A Goal, by definition, is more narrow than a Vision. A Vision is a broader or grander end state and cannot be specifically measured by Objectives, as a Goal can.

Figure 2. The Ends subject area in the Business Plans meta-model.

An Objective, on the other hand, is a statement of an attainable time-targeted and measurable Desired Result that the enterprise seeks to meet in order to directly achieve its Goals and through these, its Vision[xi]. An Objective, since it is measureable, quantifies a Goal. A Goal can be quantified by one or more Objectives, but an Objective can measure one and only one Goal. A Measurement is a specific value expressing one state of an Objective. An Objective can be expressed, usually serially over time, by one or more Measurements, but a Measurement expresses one and only one Objective.

Note from Figure 2 that a Desired Result can be composed of other Desired Results, thus creating a hierarchical structure. Since Goals and Objectives are types of Desired Result, they too can have a hierarchical structure[xii]. This is the basis for the hierarchical structure of business goals in the Business Goals Hierarchy where higher level goal instances are composed of successively lower level goal instances until we reach the leaf level of atomic goals. It should be noted that Measurements can be associated with any level of Objective and through this to any level in the hierarchy.

Business Goals Hierarchy

The Business Goals Hierarchy in Figure 3 describes Goals which the enterprise must achieve in order to accomplish its Vision. In the BGH, Goals and Measurements are shown in the same model. Typically Goals are depicted as orange “corner clipped” rectangles, and Measurements are depicted in the same model as yellow “corner clipped” rectangles[xiii].

Figure 3. A Business Goals Hierarchy (BGH).

The fact that a Measurement measures one and only one Goal is an important quality control factor and provides a clear assessment vehicle for performance indicators, as we will see. If a single Measurement is allowed to express more than one Objective and thus more than one Goal, there is no way to unambiguously trace a performance indicator using that Measurement back to the Vision of the enterprise and thus determine if it is a “key” performance indicator or not.

Of the three business motivation models (BGH, BOH and BPH) it is often advisable to start with the BGH first. Identifying a set of business goals as the first deliverable of a workshop establishes the scope early in the process and helps assure that the client receives value for their investment from the start by identifying the Ends that the client wishes to accomplish. It is the purpose of the BGH to capture and organize the Goals that will implement these Ends. However it is critically important that the goals be attainable, that measurable Objectives be set for them, and that they are vetted by the organization. There is sometimes the temptation to get the BGH over with quickly and get on with more tangible elements, but this would be a mistake. The BGH helps us to stay on track and solve the right problems for the enterprise. As other artifacts are developed it is always useful to go back to the BGH and ask yourself “Does what I am doing now help to accomplish the business goals?”

Starting with the BGH can mean either discovering the business goals, through interviews, documents, or other information gathering methods, separately or in combination. Or it could mean recording Goals that the enterprise has already identified and organizing them hierarchically.

One challenge in this process is getting participants to think “hierarchically” about business goals. Quite often business goals are not tied together in people’s minds nor in documentation in such a way that they easily roll up to higher level business goals or roll down to lower level business goals. Also, quite often business goals and objectives are not differentiated. In order to facilitate an architectural approach to business we need to often disambiguate terms that are used interchangeably. Business goals and objectives are examples of terms that need to be disambiguated in order to produce clear and executable business plans.

Means

There are three types of Means depicted in Figure 4, another portion of the business plans meta-model. There is the Mission which is the primary Means by which the enterprise plans to make its Vision operative; the Course of Action which is an approach or plan for configuring some aspect of the enterprise; and the Directive which is a specification that governs or constrains a Course of Action[xiv].

Figure 4. The Means subject area in the Business Plans meta-model.

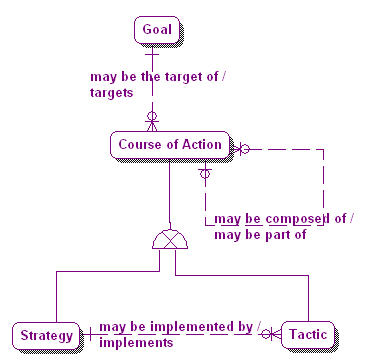

A Course of Action must be either a Strategy or a Tactic[xv]. A Strategy is the essential Course of Action attempted to carry out an enterprise’s Mission. The enterprise Mission, being the ultimate Means, can sometimes, though rarely, be carried out by more than one Strategy, especially for enterprises as vast as national governments or international corporations. For that same reason it is impossible for a Strategy to carry out more than one Mission[xvi]. A Tactic is a Course of Action that implements a Strategy by representing one or more details of that Strategy[xvii]. A Strategy can be implemented by one or more Tactics, but a Tactic is the implementer of one and only one Strategy.

A Course of Action can be composed of one or more other Courses of Action. However this compositional parent-child relationship does not cross Course of Action types. In other words, one Strategy may be a part of another Strategy, and one Tactic may be a part of another Tactic. But Tactics are separate element types from Strategies, they are implementers of Strategy, not parts of a Strategy.

The third type of Means, the Directive must be either a Business Policy or a Business Rule. A Business Policy is a non-actionable Directive that guides the activities of the enterprise or governs them in a general way. It “governs”, it does not control or shape Courses of Action[xviii]. A Business Rule is a more specific and actionable constraint on the enterprise. In particular, based on a Business Policy, it imposes a constraint on a fact or fact type[xix]. A complete look at business policies and rules includes elements that describe enforcement levels, implementations of the enforcement levels, invocations of the consequences that are the result of the enforcement level implementations, and how enforcement levels and consequences are affected by tactics. All of which are outside the scope of this article.

A Course of Action can also enable one or more other Courses of Action. Enabling is not the same as implementing. For example, a tactical Course of Action of an enterprise might be “Provide unified communication capabilities (i.e. integrated voice, email, instant messaging and video conferencing) to all employees”. This Tactic may enable the Tactic “Reduce intra-company communication delays”, which may in turn enable the Strategy “Improve company responsiveness”. Figure 5 shows the meta-model of this relationship. In it, the element Enablement implements a composite relationship between two Courses of Action. One Course of Action is the enabler of the relationship, while the other Course of Action is enabled by the relationship.

Figure 5. Enablement of Courses of Action.

Strategies and Goals

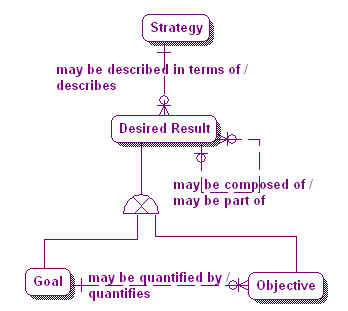

The link between an enterprise’s Ends and Means is characterized as the relationship between its Vision and Mission. A Vision may be made operative by one or more Missions, and a Mission makes operative one and only one Vision[xx]. However most business planning activity takes place at the strategic level rather than at the mission level. In making strategic decisions, an enterprise’s mission is often considered a constant set of values that the strategy must carry out. With this in mind it makes sense to model the relationship between a Strategy, which is a type of Course of Action, and the Desired Results that describe it. Figure 6 illustrates this relationship. In it a Strategy may be described in terms of one or more Desired Results, each of which is either a Goal or an Objective.

Figure 6. Strategies and Desired Results.

On the other hand a Goal, which is a type of Desired Result, may be the target of one or more Courses of Action, each of which is either a Strategy or a Tactic. This relationship is illustrated in Figure 7.

Figure 7. Goals and Courses of Action.

The basic takeaway here is that Courses of Action can be traced directly back to the Desired Results that motivate them.

Influencers and Assessments

To fully understand the meta-model of the data architecture of business plans it is necessary to understand not just its Ends and Means, but also with the real world things that influence them. These we call Influencers, where an Influencer is anything that can produce an effect on the enterprise without apparent exertion of tangible force or direct exercise of command[xxi].

The effect of Influencers on Ends and Means is determined by one or more Assessments, where an Assessment is a judgment about the implications of the Influencer either with respect to one or more Means (such as a particular Course of Action) or with respect to one or more Ends (such as a particular Desired Result)[xxii].

Figure 8 shows that portion of the meta-model that represents Influencers and Assessments. We can see that an Influencer is an example of one and only one Influencer Type. These types can be as basic as “Internal Influencer” and “External Influencer”, which tell us very little about this element, or all the way to a full taxonomy of Influencer Types, which can include all aspects of an enterprise. Influencer Types can also be nested in a supertype-subtype generalization hierarchy. A full analysis of influencers is well beyond the scope of this article. We also see that while an Assessment assesses one and only one Influencer, each Assessment must be composed of one or more Assessment Elements. Each Assessment Element, as was observed earlier, in Figure 1, must exist with respect to either one Means or one End.

Figure 8. Influencers and Assessments.

It is the Assessment Element and the fact that it may be revealed by one or more Potential Impacts on the enterprise that is the basis for the Key Performance Indicator (KPI). Figure 9 introduces the KPI into the meta-model as a type of Assessment. Because a KPI can be composed of other KPIs it has a reflexive parent-child relationship with itself. Each Assessment has its own types of Assessment Elements. Frequently encountered Assessment Elements include those used in “SWOT” analysis, such as Strengths, Weaknesses, Opportunities and Threats.

Every KPI must have at least three Assessment Elements. Target Expression, Actual Expression, and Status Expression are each a mandatory part of a KPI. In addition it can have other Assessment Elements which are optional. We will discuss these and other aspects of the data architecture and meta-model of KPIs in the second part of this article.

Figure 9. Assessments and KPIs.

Conclusion

The data architecture of business plans, also known as the Business Motivation Model, is important because it can be used to trace the results produced by Assessment Elements like Key Performance Indicators back all the way to the core motivational elements of an enterprise, its Ends and its Means. If the chain of traceable associations from Assessments like KPIs is unbroken, it is possible to architecturally trace back to the Desired Results that motivate an enterprise’s Courses of Action to understand the rationale for the Measurements used in the Assessment Elements of Key Performance Indicators that provide the most relevant picture of an enterprise’s performance. A refrain often heard in EPM projects is “Are we measuring the things that really matter?” “What are the things that will make the most difference to the enterprise?” With this two part article we will show that you can verify and validate these important associations through traceability all the way to the enterprise’s Ends and Means. In the second part of the article we will discuss how KPIs, Scorecards and Dashboards tie these elements together.

[i] I am referring to the co-ordinates of the Zachman Framework for Enterprise Architecture, first discussed in 1987, and extended in “Extending and Formalizing the Framework for Information Systems Architecture”, J.F. Sowa and J. A. Zachman, IBM Systems Journal, vol. 31, no. 3, 1992. IBM Publication G321-5488. For more on the Zachman Framework please refer to the website http://www.zifa.com/ .

[ii] Concepts in this article are based on the publications: “The Business Motivation Model, Business Governance in a Volatile World”, The Business Rules Group, Copyright 2007, The Business Rules Group, For more information refer to http://www.BusinessRulesGroup.org. This publication has since been replaced by the “Business Motivation Model, Version 1.0” published in August 2008 by the Object Management Group (OMG). For more refer to http://www.omg.org/ .

[iii] The view that there are three types of performance dashboards comes primarily from: Performance Dashboards: Measuring, Monitoring, and Managing Your Business, Wayne Eckerson, John Wiley and Son, October 2005. For more information see http://www.wiley.com/WileyCDA/WileyTitle/productCd-0471757659.html.

[iv] “Six Basic Interrogatives – Parts 1, 2 and 3, http://www.datawarehouse.com/article/?articleId=5140 .

[v] Data Model Patterns: A Metadata Map, David C. Hay, The Morgan Kaufmann Series in Data Management Systems, Morgan Kaufmann, 2006. Page 277.

[vi] Hay, Page 284.

[vii] Hay, Page 287.

[viii] Please forgive me for introducing yet another term into our ever growing business and IT vocabularies, but the metamodel of a dimensional database design would contain “meta-dimensions”, would it not?

[ix] Hay, Page 277.

[x] Hay, Page 277.

[xi] Hay, Page 277.

[xii] In object oriented terminology we would say that “Goal” is a sub-type of “Desired Result” and inherits its properties, including its relationships. In this case the relationship is an aggregation, or “part of “ relationship, with itself, creating a reflexive relationship.

[xiii] The color and symbol are arbitrary of course, but standard representations enhance readability and give the same type of artifact consistency across projects giving a type of “human resource” re-usability. After all if a consistent symbol is always used to represent the same type of thing less re-learning, is required. This also a principle of good data display, always use the same color to represent the same thing.

[xiv] Hay, Page 278.

[xv] Hay, Page 278.

[xvi] As a comment I would add that it is often when an enterprise attempts to use a strategy to accomplish more than one mission that it loses sight of the original mission of the strategy and adds unnecessary and dangerous ambiguity to that mission.

[xvii] Hay, Page 278.

[xviii] Hay, Page 280.

[xix] Hay, Page 280.

[xx] Hay, Page 276.

[xxi] Hay, Page 284.

[xxii] Hay, Page 285.

————————————————————————————————————————

In the first part of this article about the data architecture of business plans, we discussed an industry standard meta-model for modeling business motivation[i]. We started with the four core elements of business plans: End, Means, Influencer, and Assessment. We identified Desired Result as the type of End that an enterprise intends to maintain, and Goal and Objective as two types of Desired Result. We also included Measurement as an expression of an Objective. On the Means side we identified Course of Action which represents the approach or plan for configuring some aspect of the enterprise, Strategy as the essential Course of Action for carrying out the enterprise’s plan, and Tactic as the means to implement the Strategy.

An Assessment, we’ve seen, is a judgment about the impact of Influencers on the enterprise’s Desired Results and Courses of Action[ii]. Assessment Elements are the components of an Assessment that link it to individual Desired Results and Courses of Action. The net effect of an Assessment Element is the identification of a measured Potential Impact[iii].

A Key Performance Indicator (KPI) is a type of Assessment that is a judgment about the impact of the difference between two measurements, the Target Expression, associated with a Desired Result and the Result Expression, associated with a Course of Action.

Desired Results

Figure 10 illustrates the relationship between a Desired Result and a Key Performance Indicator. A Key Performance Indicator has exactly one Target Expression which is based on one and only one Objective which quantifies one and only one Goal. As we’ve already observed, both Goal and Objective are types of Desired Result. If the Desired Result is a Goal it may be quantified by one or more Objectives. Each Objective may be the basis of one or more Target Expressions. Each Target Expression is a part of one and only one KPI.

Figure 10. Desired Results and Target Expressions.

However, not all Goals are stated in a way that makes them easily quantifiable by an Objective. When a Goal cannot be quantified by a set of Objectives one of two things is bound to happen. Either the Goal becomes more or less irrelevant to the operation, productivity or culture of the enterprise and thus its significance is eventually deprecated, or Objectives that quantify it are eventually defined, vetted and socialized. There is a thin line between Goals and Objectives, as we’ve seen they are really just two types of the same thing, Desired Results. The difference between them is driven by the fact that we need a way to differentiate between Desired Results that can be measured and those that cannot. For purposes of performance management we ignore those that cannot be measured.

Courses of Action and Result Expressions

Figure 11 illustrates the relationship between a Course of Action and a Key Performance Indicator. A Key Performance Indicator has exactly one Result Expression which is based on one and only one Actual Result which is produced by one and only one Business Process which may employ one or more Efforts. Each Effort is invoked by one and only one Course of Action. However, a Course of Action may be invoked via one or more Efforts, each of which is used by one and only one Business Process. Each Business Process may produce one or more Actual Results, each which may be the basis of one or more Result Expressions. A Result Expression is a part of one and only one KPI.

Figure 11. Courses of Action and Result Expressions.

It is assumed that the Potential Impact of a KPI can be judged, usually in discrete intervals, along a continuum from very positive or very negative. What constitutes positive or negative for any KPI is determined by the requirements of the business and is subject to change over time. This fact is why configuration management of KPIs is important. Without configuration management, the ability to compare not just KPI status and trend values from period to period, but the evolution of the method by which they were calculated can be tracked. This becomes more important as organizations begin to not only use KPIs to do assessments and influence behavior, but also to judge the effectiveness of the KPIs themselves, their relevance to changing business patterns and their effectiveness in bringing attention to areas that need it. In this article however we are primarily interested in the design and construction of KPIs and not as much in how they potentially impact and are impacted by various influencers.

The Role of Effort

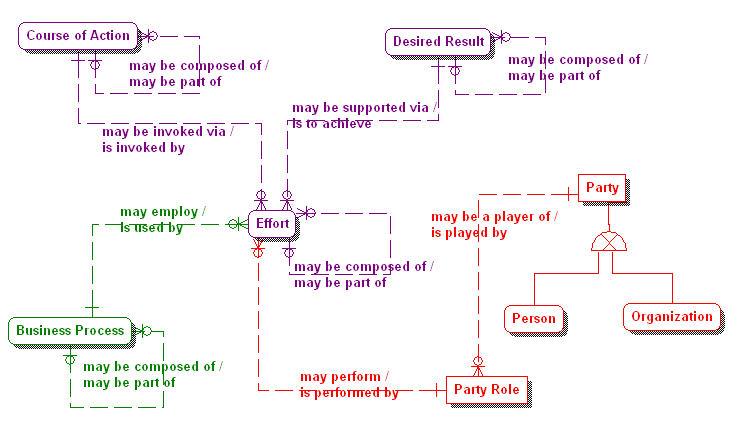

Figure 12 illustrates the central role that Effort plays in the meta-model of the data architecture of business plans. A Course of Action, as we saw in Figure 11, may be invoked via one or more Efforts. The figure also shows that a Desired Result may be supported via one or more Efforts. It shows that a Business Process may employ one or more Efforts. Finally, a Party, which is either a Person or an Organization, may be a player of one or more Party Roles, one of which then may perform one or more Efforts.

From the perspective of an Effort it is invoked by one and only one Course of Action, in order to achieve one and only one Desired Result. It is also used by one and only one Business Process while it is performed by one and only one Party Role.

Figure 12. The central role of Effort in the business plans meta-model.

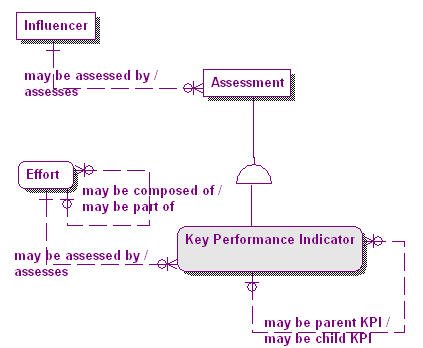

As stated earlier an Influencer is anything that can produce an effect on the enterprise without apparent exertion of tangible force or direct exercise of command[iv]. As depicted in Figure 13 we see that an Effort may be assessed by one or more Key Performance Indicators in the same way that an Influencer may be assessed by one or more Assessments. Correspondingly, a KPI assesses one and only one Effort, as an Assessment of which it is a subtype, assesses one and only one Influencer.

Figure 13. Key Performance Indicators and Influencers.

Key Performance Indicators

There are many different perspectives from which an organization’s performance can be viewed. There are also many different aspects in which each perspective on performance can be viewed. One aspect is that of motivation, or “why” has the performance turned out as it has and how can the organization improve its performance. At each perspective of the Motivation aspect[v] “why” type questions need to be answered. Answers to these questions are aided greatly by the assessments of the measurements that indicate the performance of the organization. These indicators are called performance indicators, and most organizations have a large number of them. Many of these are recorded because they “always have been” and others simply because they are relatively easy to produce. In order to provide decision makers with just the right set of performance indicators at the right time, the concept of the Key Performance Indicator (KPI) was developed. A KPI is not only an indicator of some aspect of performance but it is critical to improving that aspect of performance. It is also “key” because it can be clearly associated with a perspective of the enterprise. For example, there are KPIs that assess performance at the Planner perspective, at the Owner perspective, at the Designer or Architect perspective, at the Builder perspective, at the Subcontractor perspective, and even at the Functioning Enterprise perspective[vi]. The higher the perspective is in the enterprise architecture, the more strategic its assessments tend to be.

There are many business performance oriented books and articles that describe techniques for determining which performance indicators are Key Performance Indicators, and a study of how to select the best KPIs is beyond the scope of this article. Suffice it to say that the process is very specific to both the organization and its industry. There can be almost an unlimited number of performance indicators in any good sized enterprise. Not all performance indicators are of equal importance when it comes to assessing the performance of an enterprise. A performance indicator is said to be “key”, and thus a Key Performance Indicator when it can be demonstrated through measurements, that it is an indicator of the enterprise’s ability to accomplish its goals and objectives through the carrying out of its mission by strategic, tactical and operational means.

In this article we are interested in the data architecture of KPIs. Figure 14 illustrates the structure of a Key Performance Indicator. Since KPIs are Assessments of Effort and an Effort may be composed of other Efforts, a Key Performance Indicator may also be composed of other Key Performance Indicators.

Figure 14. The Key Performance Indicator meta-model.

In the meta-model of the business plans data architecture a Key Performance Indicator always has one each of three (3) expression elements. These are:

- Target Expression (aka Target) which is part of one and only one KPI and is based on one and only one Objective. An Objective may be the basis of more than one Target Expressions however, and thus may be used in more than one KPI.

- Result Expression (aka Result) which is part of one and only one KPI and is based on one and only one Actual Result. An Actual Result may be the basis of more than one Result Expressions however, and thus may be used in more than one KPI.

- Status Expression (aka Score) which is part of one and only one KPI and is used to indicate how the Result Expression compares to the Target Expression. It uses one Result Expression and one Target Expression. Each of which is used in exactly one Status Expression. It can take the following forms:

- A Score expressed as a percentage where the Result Expression is divided by the Target Expression, or

- A Function that returns a normalized value between -1 and 1 where 1 is interpreted as “Result is very good” and -1 is interpreted as “Result is very bad”

The Status Expression is often expressed graphically as an indicator using a set of color-coded graphic icons. For example: red, yellow or green icons to represent the different judgments made by the KPI. The specific indicator associated with the different states of the Status Expression is determined according to some Scoring Pattern and Banding Method combination, as we shall see shortly.

Figure 14 also shows the other four (4) optional elements of a KPI. These include:

- Trend Expression (Trend) which shows the directional change in the Status Expression. It can either show the change period over period, or be derived by a formula that returns a normalized value between -1 and 1 where 1 is interpreted as “Status is getting a lot better” and -1 is interpreted as “Status is getting a lot worse”.

- Weight Expression (Weight) which returns the relative weight of the KPI. If a KPI has a parent KPI you can define the weight to control the contribution of a KPI to its parent. For example, if there are two child KPIs, one weighted at 60% and the other at 40%, the parent KPI would be more influenced by the former than the latter.

- Time Expression which returns the current time dimension member that is relevant for the KPI. For example, time can be expressed either as a Point in Time indicating the KPI assesses the performance of an Event, or a duration, the difference between two points in time, to indicate performance assessment over a period of time.

- Responsible Party who is typically the person or organization responsible for the KPI. This responsibility can be for maintenance such as changing and updating any of the expression elements of the KPI. The responsibility can also be accountability for the performance of the enterprise underlying the KPI. These two responsibilities may or may not belong to the same Party. If it is the same party then issues of conflict of interest may arise. Over time, maintenance of KPIs and the Measurements on which they are based is very important. If KPIs are expected to continue to be relevant and return value to the enterprise they must be adjusted to reflect changing business conditions.

KPI Scoring and Banding

Probably the most common scoring and banding combination for Key Performance Indicators is illustrated by the example in Figures 15 and 16[vii]. This technique is referred to as “Increasing is Better – Actual Values”. In this method the higher the Score the better, with the Score determined by dividing the actual Result value by the actual Target value and expressing it as a percentage. Quite often a maximum Score value is set. Figure 2.7 illustrates this technique with five (5) component measurements rolled up into one composite measurement. The composite Score (119.95%) is simply the sum of the component Scores divided by the number of component KPIs (listed under “Measure” in the example below).

Figure 15. An example of an “Increasing is Better – Actual Values” type composite KPI.

As illustrated in Figure 16, threshold values are determined for the scoring bands of the KPI (three in this case) labeled “Good”, “Average” and “Poor”. If the Score is equal to or greater than 100%, it is assessed as “Good” and the Status indicator is a green square, if the Score is less than 100% but equal to or greater than 90% it is assessed as “Average” and the Status indicator is a yellow triangle, and finally if the Score is less than 90% it is assessed as “Poor” and the Status indicator is a red circle. KPIs for which there is no score are shown as white circles.

Trend is calculated by taking the difference between the current period Score and some previous period Score (in this case the previous month). If the difference is positive, an upward pointing “arrow in a circle” icon is displayed, if the difference is negative the arrow points downward, and if there is no change the circle icon has no arrow. Each KPI has a name, in this case “Administration” and a description (not shown). They are grouped into both Program and Strategic Scorecards which can then be incorporated into operational, tactical and strategic dashboards.

Figure 16. An example of a Scorecard with KPI scoring bands.

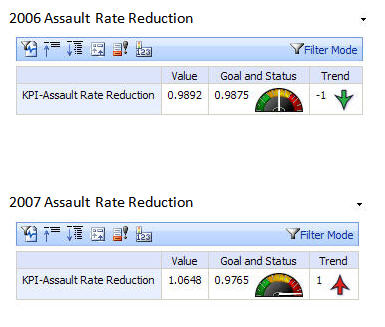

For performance assessment problems requiring more complex calculations, expressions are used instead of raw values when comparing the Result value to the Target value. This is a technique available in many BI and enterprise performance management (EPM) tools today. Rather than using the raw Target and Result values to calculate a Score, the results of a Target Expression and a Result Expression are factors in the calculation of a Status Expression. The two KPIs in Figure 17, though more simple in appearance, are intuitive in design and actually represent more complex calculations than the previous example.

The challenge here is to assess the performance of an institution in reducing criminal assaults cumulatively over a number of years. The top KPI represents performance for 2006 and the bottom for 2007. The Desired Result is stated in terms of the number of assaults per population of 1,000, the strategic Goal is to reduce assaults by 5% over a four year period, so the tactical Objective is to decrease the percentage by 1.25% each year. A Target Expression is used to calculate the Target value (labeled as “Goal”) applying each year’s percentage reduction to the previous year’s Target value thus producing a progressively aggressive Target.

The Actual Result produced by the Business Process is calculated by a Result Expression and expressed as a Result value (labeled “Value”). For 2006 the Result is 0.9892 and the Target is 0.9875, which is 1.25% less than the Target for 2005. This performance is assessed as “Average” by the Status Expression and banded with a yellow Status indicator (the middle yellow segment of the dial icon). The Trend is downward, i.e. there were fewer assaults in 2006 than in 2005, and thus the Trend indicator (the arrow) is pointed downward, and this is better than the previous period (2005) so the Trend indicator arrow is green. This is an example of a “Decreasing is Better – Actual Values” type of KPI.

In 2007 the Target is decreased to 0.9765 per 1,000 population, making the criteria for the “Good” and “Average” performance bands more stringent to meet. In the bottom KPI we see that the Actual value is 1.0648 thus pushing the Status indicator into the “Poor” band (the right-hand red segment of the dial icon) and causing the Trend indicator to point upward, because of the increase in Actual value and turn red because of the increase in percentage, calculated by the Result Expression, over the 2006 percentage.

Figure 17. An example of a “Decreasing is Better – Actual Values” type of complex KPI.

The Trend icon is an example of the use of one graphic icon to display two measurements. The direction of the arrow indicates the direction of the Trend, up or down, and the color indicates the judgment of that direction expressed, green for “Good” and red for “Poor”. The can be confusing in not explained. Also the use of color alone to indicate a state of performance means that about 10% of the adult population cannot discern its meaning because of color blindness. The example above is used to indicate a concept not necessarily to indicate best KPI display practices.

Scoring Patterns and Banding Methods

The Scoring Pattern of a KPI (as seen above) indicates whether it is better to have a Result that is increasing, decreasing, or as close to the Target as possible, without being either higher or lower. The table below describes the three KPI Scoring Patterns.

|

Scoring Pattern |

Assessment Criteria |

| Increasing is Better | In general, the greater the value of the Result the better. Usually if the Result is greater than the Target it is considered to be a positive condition. For example, under most circumstances it is considered better to have increasing revenue. KPIs assessing revenue topics are generally banded as “Increasing is Better”. |

| Decreasing is Better | In general, the less the value of the Result the better. Usually if the Result is less than the Target it is considered to be a positive condition. For example, under most circumstances it is considered better to have decreasing costs. KPIs assessing cost topics are generally banded as “Decreasing is Better”. |

| Closer to Target is Better | In general, the closer the Result is to the Target the better. Usually if the Result is exactly the same value as the Target it is considered to be a positive condition. For example, under most circumstances meeting headcount targets as close as possible in a given period is considered better than either hiring too few people or hiring too many people. |

The Banding Method determines if actual values, normalized scale values or some other method is to be used to arrive at the Result value and Target value. Banding Method however does not determine how many bands are used. Many KPIs use three scoring bands because it is the simplest way to convey the relationship between a Target Expression and a Result Expression. The table below describes three KPI Banding Methods.

|

Banding Methods |

Assessment Criteria |

| Actual Values | Banding is done using the quotient of the Actual value divided by the Target value which is referred to as the Score. |

| Normalized Actual over Target | Banding is done using a Function that returns a normalized value between -1 and 1 where 1 is interpreted as “Result is very good” and -1 is interpreted as “Result is very bad”. |

| Stated Score | An advanced technique where stated scores may be systematically substituted for Actual and Target values. |

Summary

In this article we have attempted to show a way to extend the data architecture of business plans from the Ends and Means of the Business Motivation Model[viii] all the way to the Key Performance Indicator, a widely used Assessment tool for determining the success or failure of those plans.

[i] “Business Motivation Model, Version 1.0” published in August 2008 by the Object Management Group (OMG). For more refer to http://www.omg.org/ .

[ii] Influencers can have an impact on other types of Ends such as the enterprise’s Vision, and other types of Means like Mission and Directive as well.

[iii] Hay, Page 187.

[iv] Hay, page 187.

[v] The Zachman Framework for Enterprise Architecture.

[vi] See earlier references to the Perspectives of the Zachman Framework for Enterprise Architecture.

[vii] Courtesy of the “Boston About Results” program, Boston, MA, USA.

[viii] The Business Motivation Model, Business Governance in a Volatile World, The Business Rules Group, Copyright 2007, The Business Rules Group.

June 10, 2018 at 2:05 pm |

[…] of motivators entitled “The Data Architecture of Business Plans”[i] which can be found at https://birkdalecomputing.com/6bi-home/the-data-architecture-of-business-plans/ […]

September 30, 2019 at 5:54 am |

Do you mind if I quote a few of your articles as long as I provide credit and sources back to your blog? My blog site is in the very same area of interest as yours and my visitors would really benefit from a lot of the information you provide here. Please let me know if this okay with you. Appreciate it!

October 14, 2019 at 2:55 pm |

Feel free to quote anything from my web site as long as you include my name and blog site as the source.